Session 17: Optimal Financing Mix I - The Trade Off

Trade-off Between Debt and Equity in Corporate Finance

Introduction to Debt vs. Equity

- The session focuses on the trade-off between using debt and equity for financing, highlighting advantages like tax benefits of borrowing and disadvantages.

- This discussion is part of a broader exploration of corporate finance principles, specifically the financing principle regarding optimal capital structure.

Understanding Debt and Equity

- The session aims to establish the right mix of debt and equity for companies, addressing both components of the financing principle.

- Key distinctions between debt and equity include:

- Debt has a contractual fixed claim while equity has a residual claim.

- Debt payments are typically tax-deductible; equity payments usually are not.

- In bankruptcy, debt investors have priority over equity investors.

Characteristics of Debt vs. Equity

- Investors in debt do not influence company operations, whereas equity investors often do.

- Debt generally has a finite maturity compared to equity which does not expire.

- Examples include:

- Bank loans and corporate bonds as clear forms of debt.

- Various types of equity such as personal savings or venture capital.

Defining Debt Ratios

- The speaker defines "debt ratios" as the proportion of debt relative to overall capital (debt / (debt + equity)), typically expressed in market value terms.

- An example given: an optimal debt ratio might be stated as 20%, indicating that this percentage reflects market value rather than book value.

Analysis of Company Debts

- Four companies analyzed: Disney, Tata Motors, Baidu, and Bookscape with varying structures in their debts.

- Disney's primary form of debt is corporate bonds; U.S. companies historically rely more on this than international counterparts.

Maturity and Currency Breakdown

- Disney holds significant short-term (13%) and long-term debts; Tata Motors has longer-term obligations due to project lifespans typical in mining industries.

- A notable point about Disney’s currency breakdown shows it predominantly uses U.S. dollar-denominated debts despite having international operations.

Evaluating Optimal Mixes

- The analysis seeks to determine if these companies' mixes of debt and equity are appropriate for their operational contexts.

Corporate Lifecycle Considerations

Understanding Debt Capacity and Its Implications

The Lifecycle of a Company and Debt Capacity

- As a company's growth levels off, it begins to generate earnings without needing significant reinvestment, leading to increased debt capacity.

- Initially, companies may not utilize their full borrowing potential; however, as they mature, they start to borrow more due to increased debt capacity.

- A company's lifecycle stage can predict its expected debt ratio; this is a simplistic yet effective way to assess the right mix of debt and equity.

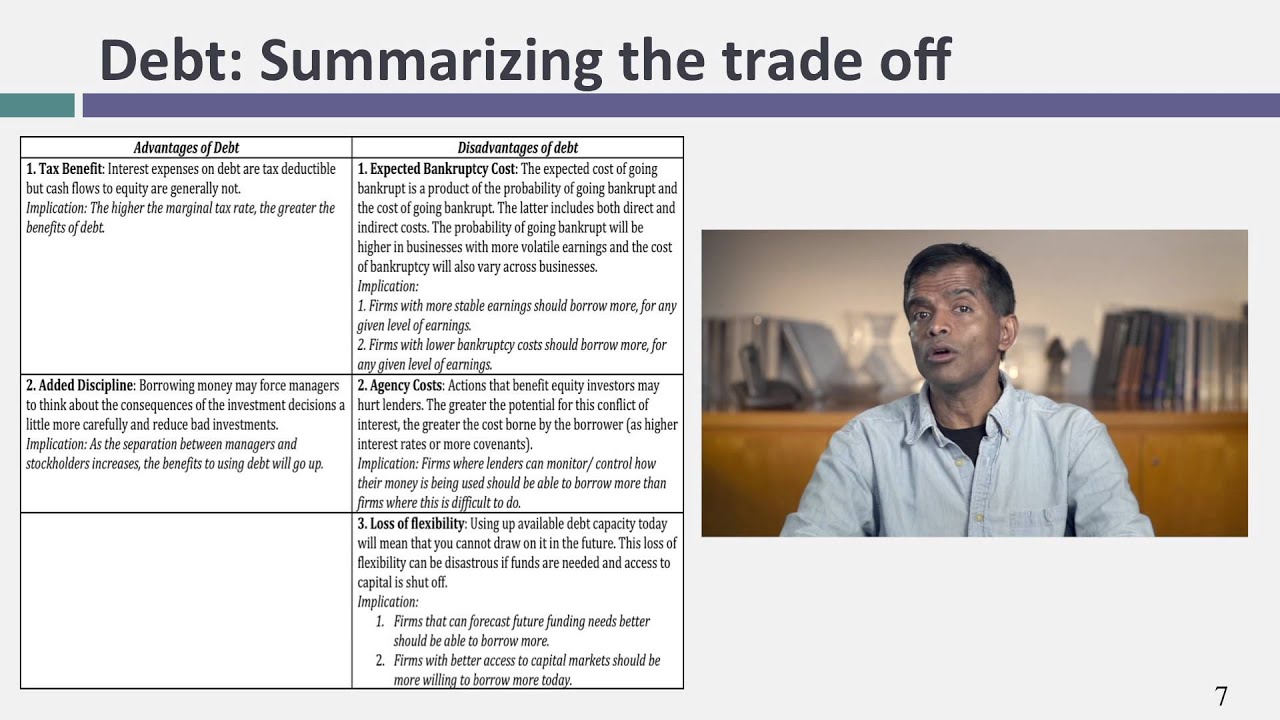

Trade-offs of Using Debt vs. Equity

Benefits of Debt Financing

- Two major benefits of using debt over equity include tax advantages (interest is tax-deductible) and added managerial discipline.

- Companies in higher marginal tax rate countries (e.g., the US, Japan) should leverage more debt compared to those in lower tax rate countries (e.g., Ireland).

Added Discipline from Borrowing

- Managers of primarily equity-funded companies may become complacent; borrowing money imposes interest obligations that encourage better project selection.

- Increased borrowing creates consequences for poor project choices, potentially leading to job loss or bankruptcy if interest payments cannot be met.

Costs Associated with Debt Financing

Expected Bankruptcy Costs

- The probability of bankruptcy increases with additional borrowing; even large firms like ExxonMobil face heightened risks when taking on more debt.

- Direct costs associated with bankruptcy can be substantial, often amounting to 30%-40% of a company's assets once declared bankrupt.

Indirect Costs and Agency Issues

- Indirect costs arise when stakeholders perceive financial trouble—customers may stop buying products, suppliers demand cash upfront, and employees seek other jobs.

- Agency costs reflect conflicts between equity investors' interests (riskier projects for higher returns) versus lenders' preferences for stability.

Loss of Flexibility

Tax Benefits and Debt Ratios Across Companies

Tax Benefits from Debt

- Disney is expected to gain the largest tax benefit from debt due to higher marginal tax rates compared to other companies.

- Baidu, with a lower marginal tax rate in China, will have a smaller tax benefit; Tata Motors falls in between with a 29.5% or 32.5% tax rate.

- Brazil's unique tax law provides partial reductions for cash flows to equity, resulting in Valiant having the smallest overall tax benefits among the companies discussed.

Added Discipline from Borrowing

- Disney is anticipated to receive significant benefits from borrowing due to its separation of stockholders and managers, allowing for better oversight on project selection.

- Baidu's young company structure allows its founder CEO to monitor management closely, while Tata Motors' family group ownership reduces the need for borrowing discipline.

Expected Bankruptcy Costs

- Baidu faces high expected bankruptcy costs as a tech company reliant on uncertain future growth.

- Tata Motors and Valiant experience earnings volatility due to cyclical nature and commodity price fluctuations respectively, increasing their bankruptcy risk.

- Disney’s diversified entertainment model leads to more stable earnings, enabling it to afford higher levels of debt.

Agency Costs and Future Flexibility

- Baidu likely has the highest agency costs due to intangible assets; Tata Motors and Valiant have lower agency costs owing to physical assets.

- As a growth company, Baidu values future flexibility highly; however, other mature companies are more stable regarding future investment needs.

Trade-offs in Debt Decisions

- The discussion emphasizes that Disney may have the highest debt ratio while Baidu might maintain the lowest due to varying factors like stability and growth potential.

- Evaluating any company's expected benefits from debt involves analyzing marginal tax rates and management structures alongside potential bankruptcy and agency costs.

Hypothetical Scenario: No Taxes or Bankruptcy

- In an ideal world without taxes or bankruptcies where managers act correctly, there would be no need for added discipline or concern over agency costs.

Understanding the Modigliani-Miller Theorem

Overview of the Theorem

- The Modigliani-Miller theorem posits that in a world devoid of taxes and default risk, borrowing amounts (e.g., $100 million or $1 billion) yield no benefits or costs. This suggests that capital structure does not affect firm value under these ideal conditions.

- For the theorem to hold true, it is essential that there are no taxes, default risks, or agency costs. While this scenario is unrealistic, it serves as a foundational concept for understanding when debt may not influence corporate finance.

Implications of the Theorem

- In an idealized environment described by the theorem, changing a company's debt ratio does not alter its cost of capital or overall value. This indicates that firms can operate effectively regardless of their leverage levels.

- A common takeaway among business students regarding capital structure lectures is often limited to remembering the Modigliani-Miller theorem itself. However, many overlook its underlying assumptions about taxes and risks.

Real-world Considerations