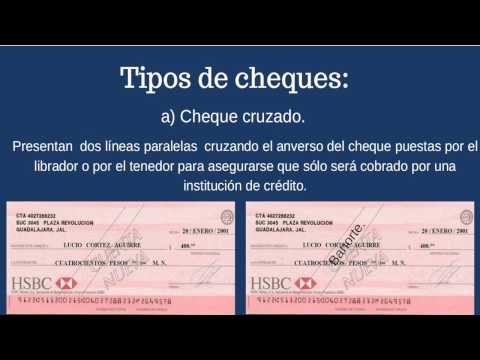

Tipos de cheques

Types of Cheques in Credit Operations Law

Overview of Cheques

- The discussion begins with the types of cheques defined by the General Law on Titles and Credit Operations, starting with Article 197.

- Focus is placed on crossed cheques, which feature two parallel lines across the front, indicating that they can only be cashed by a credit institution.

Crossed Cheques

- There are two types of crossed cheques: general and special. A general crossed cheque does not specify a particular institution between the lines, allowing any credit institution to cash it.

- In contrast, a special crossed cheque includes the name of a specific institution between the lines; it can only be cashed by that designated institution or an endorsed party.

Transformations and Validity

- A general crossing can be transformed into a special crossing by adding an institution's name; however, once established as special, it cannot revert to general.

- Any alterations to remove crossings or names are invalid. While these cheques can circulate through endorsement, payment will only occur if presented by another credit institution.

Practical Example of Crossed Cheque Usage

- An example illustrates how parents might use a crossed cheque for their child's tuition payments to ensure funds go directly to the educational institution rather than being given in cash.

Certified Cheques

- The conversation shifts to certified cheques. Before issuing one, the drawer may request certification from their bank confirming sufficient funds are available for payment.

- Certified cheques are often required for government transactions like tax payments because they guarantee that funds will be available when presented for cashing.

Responsibilities and Limitations

- Upon certification, responsibility shifts from the drawer (e.g., Jé López in this case) to the bank regarding payment obligations.

Cheque Certification and Its Implications

Understanding Cheque Certification

- The certification document has the same legal effect as the acceptance of a promissory note, releasing the drawer from obligations. The bank becomes directly liable upon certification.

- A cheque can be certified through a simple signature or by stating "accepted" or similar phrases, making it less formalistic. The drawer can revoke a certified cheque if returned for cancellation.

- The primary purpose of a certified cheque is to assure the beneficiary that the amount will be paid when presented at the bank, providing security in transactions such as rental agreements.

Advantages of Certified Cheques

- In competitive rental situations, landlords may require certified cheques to ensure payment reliability from prospective tenants.

- Certified cheques mitigate risks for landlords by guaranteeing that funds are available when presented, preventing complications with multiple interested parties.

Special Types of Cheques: "Para Bono en Cuenta"

- A "para bono en cuenta" cheque cannot be cashed but must be deposited into an account designated for the beneficiary. This clause prevents cash payments and ensures secure transactions.

- Once this clause is included, the cheque becomes non-negotiable; it cannot be endorsed but can only be transferred through ordinary assignment methods.

Practical Applications and Limitations

- Such cheques serve practical purposes in legal contexts where clients may need to transfer payments securely without risking improper endorsements.

- Including "para bono en cuenta" on a cheque allows individuals to delegate deposit responsibilities while ensuring funds are credited correctly to specified accounts.

Bank Responsibilities and Regulations

- Banks are mandated by law to process these types of cheques according to their stipulations, ensuring compliance with regulations regarding payment methods.

- If there’s any irregularity in payment processing, banks hold responsibility under legal frameworks governing these financial instruments.

Understanding Cashier's Cheques

Definition and Usage

- A cashier's cheque is issued by a financial institution and is payable at its own branches or affiliates. It serves as a secure form of payment often required for significant transactions like tuition fees.

Acquisition Process

- To obtain a cashier's cheque, one must present identification. Customers with accounts can have amounts deducted directly from their balance plus any applicable fees.

Cheque de Caja y su Funcionamiento

Características del Cheque de Caja

- El cheque de caja se expide a favor de una persona determinada, es nominativo y no negociable, lo que significa que no puede ser endosado ni transferido a otra persona.

- Solo el beneficiario indicado en el cheque puede cobrarlo o depositarlo. En caso de robo o extravío, no puede ser cobrado por nadie más.

- Si se cancela un cheque de caja, el banco no reembolsará la comisión ya que el servicio fue prestado. La cancelación requiere presentar un documento en el banco.

Uso del Cheque Ventanilla

- En situaciones urgentes, como un accidente menor, los involucrados pueden acordar ir al banco para solicitar un cheque ventanilla si no tienen efectivo disponible.

- Este tipo de cheque permite obtener efectivo el mismo día y en la misma sucursal donde fue emitido, facilitando transacciones rápidas sin esperar a las autoridades.

- Es útil cuando se necesita dinero en efectivo urgentemente y se carece de chequera o tarjeta.

Cheques de Viajero: Seguridad y Uso

Características del Cheque de Viajero

- Los cheques de viajero son expedidos por el librador y son pagaderos en bancos o comercios autorizados tanto dentro como fuera del país.

- Al comprar cheques de viajero, deben firmarse con tinta permanente para asegurar su reembolso en caso de pérdida o robo.

- Al usarlos en el extranjero, es necesario contrafirmar los cheques para validar la operación; esto implica cotejar firmas con un empleado del establecimiento.

Endoso y Flexibilidad

- Si no se viaja debido a imprevistos, los cheques pueden ser endosados a otra persona. Esto permite que alguien más cobre los cheques si es necesario.

Cheque No Negociable: Definición y Limitaciones

Naturaleza del Cheque No Negociable

- Un cheque es considerado no negociable si incluye una cláusula específica o por disposición legal; solo puede ser endosado a una institución financiera para su cobro.

Proceso y Restricciones

- La ley establece que estos cheques solo pueden cobrarse directamente en ventanilla o depositarse en la cuenta designada.