The Trillion Dollar Equation

The Impact of a Single Equation on Financial Markets

The Birth of Derivatives and Their Influence

- A single equation has led to the creation of four multi-trillion dollar industries, fundamentally changing how people perceive risk in finance.

- Most individuals are unaware of the scale and utility of derivatives in financial markets.

Jim Simons: A Mathematician's Success in Investing

- Jim Simons established the Medallion Investment Fund in 1988, achieving an extraordinary annual return of 66% over 30 years.

- An investment of $100 in 1988 would have grown to approximately $8.4 billion today, making Simons the wealthiest mathematician ever.

Isaac Newton's Financial Missteps

- Despite his mathematical prowess, Isaac Newton lost a significant portion of his wealth by investing in the South Sea Company during its peak.

- Newton's failure stemmed from emotional decision-making; he bought shares at their peak instead of selling when he should have.

Louis Bachelier: Pioneer of Mathematical Finance

- Louis Bachelier is recognized as a pioneer for using mathematics to model financial markets, influenced by his experiences at the Paris Stock Exchange.

- He studied options contracts, which date back to ancient Greece with Thales' execution of what is considered the first call option.

Understanding Options: Call and Put Options Explained

- A call option allows buying an asset at a predetermined price (strike price), while a put option allows selling it at that price.

- Example: If Apple stock is $100 now and you buy a call option for $10 with a strike price also set at $100, your profit potential increases if stock prices rise above this level.

Advantages and Risks Associated with Options Trading

- Options limit downside risk; losses are capped to what was paid for the option rather than full stock value loss.

- They provide leverage; small investments can yield large returns but also come with higher risks compared to direct stock ownership.

Understanding the Chaos of Stock Options

The Challenge of Pricing Options

- Options are a complex investing tool, historically plagued by chaotic pricing methods where traders negotiated prices without a solid mathematical foundation.

- Bachelier proposed to explore a mathematical solution for option pricing as his PhD topic, despite the unconventional nature of finance mathematics at that time.

Market Dynamics and Randomness

- Stock prices fluctuate based on buyer-seller dynamics influenced by various unpredictable factors like weather and politics, making accurate predictions nearly impossible.

- The Efficient Market Hypothesis suggests that in an efficient market, one cannot profit from trading due to the randomness inherent in stock price movements.

Predictive Limitations in Trading

- If traders could predict future stock prices accurately, their actions would alter those prices immediately, demonstrating that predictions can affect outcomes.

Visualizing Random Walks with Galton Board

- A Galton board illustrates random walks; each ball's path is unpredictable individually but collectively forms a normal distribution over time.

- Bachelier likened stock price movements to balls on a Galton board, suggesting that expected future prices follow a normal distribution centered around current values.

Historical Context: Brownian Motion and Its Implications

- Bachelier's work rediscovered principles related to heat radiation described by Fourier, which later contributed to understanding Brownian motion observed by Robert Brown in 1827.

Understanding Diffusion and Option Pricing

The Concept of Diffusion

- Microscopic particles spreading out is defined as diffusion, which was crucial in solving the Brownian motion mystery. Einstein provided evidence for the existence of atoms and molecules, although he was unaware that Bachelier had discovered the random walk five years earlier.

Bachelier's Contribution to Option Pricing

- After completing his PhD, Bachelier developed a mathematical method for pricing options. He explained that with a call option, if a stock's future price is below the strike price, the buyer loses their premium.

- If the stock price exceeds the strike price, buyers profit from the difference. The probability of making a profit depends on whether the stock price increases beyond what was paid for it (green shaded area), while sellers benefit if prices remain low (red shaded area).

- Bachelier determined that an option's fair price should equalize expected returns for both buyers and sellers. This insight allowed him to accurately price options and solve long-standing issues faced by traders.

Lack of Recognition for Bachelier

- Despite his groundbreaking work, Bachelier went unnoticed; physicists were uninterested and traders unprepared due to a lack of significant financial incentives at that time.

Ed Thorpe: From Blackjack to Stock Market Success

Thorpe’s Innovative Strategy

- In the 1950s, Ed Thorpe utilized his skills in card counting at blackjack tables in Las Vegas to gain an advantage by tracking cards played with single decks.

- His success led him to apply these strategies in finance by starting a hedge fund that achieved remarkable annual returns of 20% over two decades.

Dynamic Hedging Explained

- Thorpe introduced dynamic hedging techniques based on mathematical principles. By assessing winning and losing odds, he could tilt outcomes favorably through strategic transactions.

- For example, if Bob sells Alice a call option when her stock is "in-the-money," he can mitigate risk by owning one unit of stock—offsetting potential losses from fluctuating prices.

Advancements Beyond Bachelier’s Model

- A hedge portfolio can offset an option's value using stocks dynamically adjusted according to current market conditions.

The Evolution of Option Pricing Models

Early Strategies and Personal Use

- The speaker discusses a model from 1967 that he initially used privately for his own investments, aiming to generate profits for himself and his investors.

- His strategy involved buying options when undervalued and short selling when overvalued, leading to frequent successful trades until 1973.

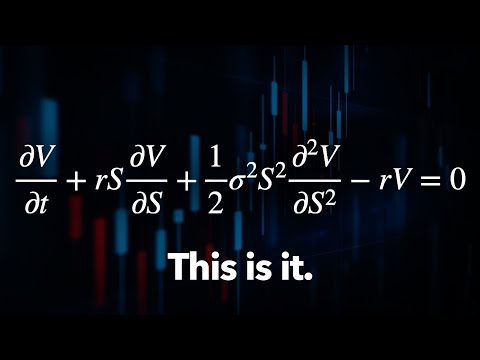

The Black-Scholes Revolution

- In 1973, Fischer Black and Myron Scholes introduced a groundbreaking equation that transformed the finance industry; Robert Merton also contributed independently with stochastic calculus.

- The speaker reflects on their superior mathematical approach compared to his own, acknowledging their model's effectiveness in pricing options fairly for both buyers and sellers.

Risk-Free Portfolio Concept

- Black, Scholes, and Merton proposed constructing risk-free portfolios using options and stocks, suggesting these should yield returns equivalent to risk-free assets like US treasury bonds.

- They built upon Bachelier's model to describe stock price movements as random with an upward or downward drift.

Impact of the Black-Scholes Equation

- Solving the partial differential equation provided an explicit formula for option pricing based on various input parameters, enabling practical trading applications.

- Within years of its introduction, the Black-Scholes formula became Wall Street's benchmark for trading options, contributing to a multi-trillion dollar industry.

Broader Applications of Options

- The framework opened new avenues for hedging risks not only for hedge funds but also large corporations and individual investors against specific financial threats.

- An example is given where airlines can hedge against rising oil prices by purchasing options linked to oil price fluctuations.

GameStop Case Study

- The GameStop phenomenon illustrated how retail investors utilized options strategically against hedge fund short-sellers through platforms like Reddit’s r/wallstreetbets.

- This leverage allowed small investors to control larger amounts of stock than they could directly purchase with cash.

Size of Derivatives Markets

- Derivatives markets are estimated at several hundred trillion dollars globally; derivatives derive value from underlying securities such as options.

- The discussion highlights the paradox where more money is invested in derivatives than in the actual underlying assets.

Market Dynamics and Derivatives

The Role of Markets in Stability

- Individuals have varying risk-reward preferences, leading to different market behaviors. This raises the question of whether these variations contribute to market stability or instability.

- In normal conditions, markets provide significant liquidity and stability. However, during periods of stress, all securities may decline simultaneously, potentially causing major market crashes.

Historical Context and Key Figures

- Merton and Scholes received the Nobel Prize in Economics in 1997 for their work on option pricing; Black was acknowledged posthumously. Their findings led hedge funds to seek new methods for identifying market inefficiencies.

- Jim Simons transitioned from a successful academic career in mathematics to finance by founding Renaissance Technologies in 1978, aiming to leverage machine learning for stock market pattern recognition.

Data Gathering and Methodology

- In the early days at Renaissance Technologies, data collection was manual; they sourced historical interest rates directly from the Federal Reserve due to a lack of digital records.

- Simons prioritized hiring PhD-level scientists from fields like physics and mathematics rather than finance professionals, believing that scientific expertise could yield better insights into complex market dynamics.

Innovations in Financial Models

- Leonard Baum's development of Hidden Markov models exemplifies how unobservable factors can influence observable outcomes—an approach applied successfully within Renaissance’s strategies.

- The Medallion Fund launched by Renaissance became renowned for its exceptional returns, prompting discussions about the validity of the efficient market hypothesis as outlined by Bradford Cornell.

Challenging Established Theories

- Research indicated that predictability exists within stock markets, contradicting traditional views that suggest markets are entirely efficient.