Basic Concept of Accounting By Saheb Academy - Class 11 / B.COM / CA Foundation

Introduction

In this video, the basic concepts of accounting are discussed. The speaker explains what accounting is, why it's important, and how it works.

What is Accounting?

- Accounting is the process of recording, classifying, and summarizing financial data into a meaningful format.

- Financial data generated from daily transactions needs to be recorded properly and classified in a structured format.

- The financial data must make sense to users such as management, shareholders or owners of the business, government or creditors so that they can take meaningful decisions based on that information.

- The two main formats for summarizing financial data are balance sheets (which give us information about the financial position of a company), and profit and loss accounts (which give us information about the financial performance of a company).

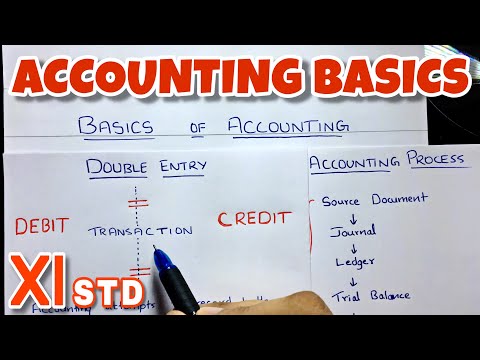

The Accounting Process

- The accounting process starts with source documents which provide evidence of transactions such as invoices or bills.

- Based on these source documents, journal entries are made in a journal book.

- Ledger accounts are then created from these journal entries through posting.

- Balances from ledger accounts are transferred to trial balances which summarize all balances. Finally, financial statements such as balance sheets and profit and loss accounts are prepared.

Conclusion

Accounting is an essential process for any business that involves recording, classifying and summarizing financial data into meaningful formats. It helps stakeholders make informed decisions based on accurate information. The accounting process starts with source documents which lead to journal entries being made, ledger accounts being created, and balances being transferred to trial balances. Finally, financial statements are prepared.

Introduction to Accounting and Financial Statements

In this section, the speaker introduces the concept of accounting and explains the accounting process. The five elements of financial statements are also discussed in detail.

Accounting Process

- Bookkeeping is the process from source document till trial balance.

- A normal accountant will do this job.

- The entire accounting process is based around five things: asset, expense, liability, equity or capital, revenue or income.

Five Elements of Financial Statements

- In accounting, there are only five things: asset, expense, liability, equity or capital, revenue or income.

- These elements are represented on the face of the financial statement.

- Expense and revenue are shown on the profit and loss statement.

- Asset, liability and equity or capital are shown in the balance sheet.

Meaning of Asset

- An asset is a resource controlled by an entity as a result of past events.

- Future economic benefits are expected to flow to the entity from that resource.

- Control means either ownership or lease basis where future economic benefit can be utilized.

Meaning of Expense

- Expense is the cost of operations that a company incurs to generate revenue.

- No further benefit is expected from it after it has been incurred.

Expense, Liability and Equity

In this section, the speaker explains the meaning of expense, liability and equity in accounting.

Expense

- An expense is a cost of operations that a company incurs to generate revenue. It is something for which the benefit has already been taken and no further benefit is expected.

- Expenses include rent, electricity bills, salaries of workers etc.

- If you pay an electricity bill, it means you have consumed the electricity. You are not going to get any more electricity from that money itself.

- The amount paid towards expenses is considered as an expense for the company.

Liability

- A liability is a present obligation of the entity to transfer an economic resource as a result of past event.

- It means there has to be an obligation on the entity (company) to pay something or abstain from doing something beneficial.

- For example, if you purchase goods worth 10,000 on credit and didn't pay then you have a present obligation to pay that person (creditor).

- The creditor will have claim on your total assets of the company.

Equity or Capital

- Capital is the money invested by owners into business.

- In case of simple partnership business it's called capital but in case of companies with thousands of shareholders it's called equity.

- Capital/equity represents ownership interest in a business.

Understanding Capital

In this section, the speaker explains what capital is and its technical definition.

Definition of Capital

- Capital is the money invested by the owners of a company.

- The technical definition of capital is the residual interest in the total assets of the entity after deducting all its liabilities.

- The claim of owners in the total asset of the company after deducting all its liabilities.

Residual Interest

- Equity shareholders get whatever is left after paying off liabilities.

- Liability holders have first claim on assets, while owners have second claim.

Understanding Revenue

In this section, the speaker explains what revenue is and how it's calculated.

Definition of Revenue

- Revenue is income - gross inflow of cash or receivables from sales, rendering services, interest received, rent received, dividends received etc.

Example Calculation

- A sole proprietorship business started with 1 lakh capital.

- Cash investment = 1 lakh

- Capital = 1 lakh

- Cash investment becomes an asset because it's controlled by an entity and has future economic benefit.

Understanding Capital and Liabilities

In this section, the speaker explains the concepts of capital and liabilities in accounting.

Definition of Capital

- The total asset of a company is owned by its owners.

- When a company purchases an asset, it becomes their property and is considered an asset because they have control over it and expect future economic benefits from it.

Definition of Liabilities

- A liability is a present obligation to transfer an economic resource as a result of past events.

- When a company takes out a loan, they receive cash but also create an obligation to pay back that loan. This obligation is considered a liability.

Relationship between Capital and Liabilities

- Both capital and liabilities are included in the balance sheet of a company.

- Liability holders have priority over owners in terms of claims on the total assets of the company.

- Owners' claim on the total assets is equal to the total assets minus all liabilities. This residual interest is known as capital.

Understanding Assets and Double Entry

In this section, the speaker explains what an asset is and introduces the concept of double entry in accounting.

Definition of Asset

- An asset is something that generates income or revenue.

- Examples of assets include cash and machinery.

Introduction to Double Entry

- Double entry is a methodology used in accounting to record two aspects of every transaction.

- Every transaction has two effects: debit and credit.

- Debit and credit represent the duality principle or dual aspect principle of accounting.

- The effects of debit and credit are always equal, which is known as the duality principle.

Understanding Debit and Credit in Accounting

In this section, the speaker explains what debit and credit mean in accounting.

Meaning of Debit and Credit

- Debit and credit are abstract terms used in accounting to represent something.

- They do not have a specific meaning on their own but relate to assets, liabilities, equity, revenue, or expenses.

- Debit does not mean plus or good while credit does not mean minus or bad.

Relationship between Debit/Credit and Dual Aspect Principle

- The dual aspect principle means that every transaction affects at least two accounts with equal amounts but opposite debits/credits.

- For example, when purchasing machinery for $20k with cash:

- Cash account decreases by $20k (credit)

- Machinery account increases by $20k (debit)

Applying Double Entry to Transactions

In this section, the speaker demonstrates how double entry works using examples.

Example Transaction

- When getting a loan from a bank for $40k:

- Cash account increases by $40k (debit)

- Loan account increases by $40k (credit)

Dual Aspect Principle in Transactions

- Every transaction has two aspects: debit and credit.

- The effects of debit and credit are always equal, which is known as the duality principle.

- Double entry ensures that both aspects of a transaction are recorded.