Sistema de amortización de préstamos FRANCÉS, ALEMÁN y AMERICANO

Understanding Loan Amortization Methods

Introduction to Loan Amortization

- The video introduces the concept of loan amortization, which refers to paying off a bank loan in installments that can be either variable or fixed.

- It highlights the three main methods of amortization: French system, German system, and American system, discussing their differences and suitability based on specific situations.

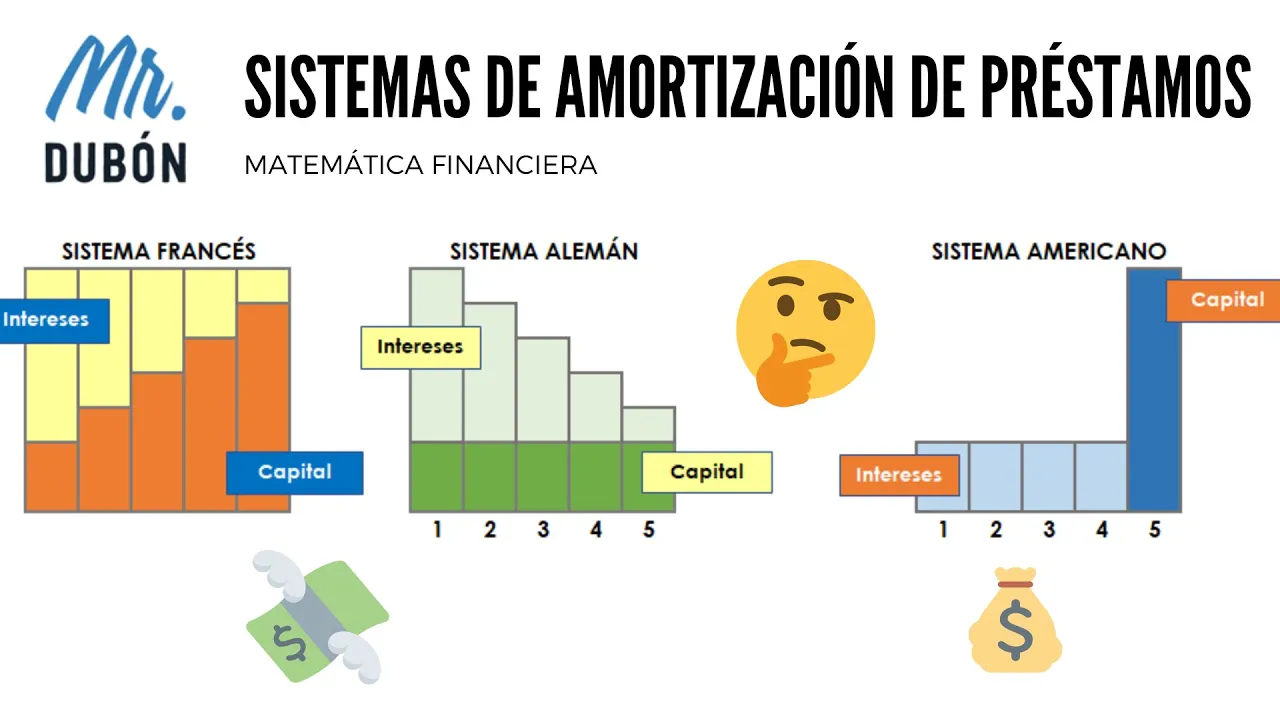

French Amortization System

- The focus shifts to the French amortization method, characterized by fixed or level payments throughout the loan term.

- Key features include:

- Fixed payment amount across all periods.

- Higher interest payments in initial periods that decrease over time.

- Capital repayments are lower at the beginning and increase towards the end of the term.

Calculating Payments

- To create an amortization table, essential data includes:

- Loan amount (e.g., $225,000)

- Annual interest rate (e.g., 28%)

- Loan duration (e.g., 5 years)

- Payment frequency (typically monthly).

- The formula for calculating level payments is introduced:

[

textPayment = fractextCapital times textInterest Rate1 - (1 + textInterest Rate)^-textPeriods

]

Practical Calculation Using Excel

- The speaker opts to use Excel's PMT function for simplification instead of manually applying complex formulas.

- Clarifies that dividing the annual interest rate by 12 aligns with local banking practices regarding conversion frequency.

Example Calculation

- For a loan of $225,000 at an annual rate of 28% over five years with monthly payments:

- Results in a level payment of approximately $700.05 per month.

- This consistent payment remains unchanged throughout all periods.

Interest and Capital Repayment Breakdown

- To calculate interest for each period:

- Use the formula:

[

textInterest = textCapital times textInterest Rate

]

- Initial calculations show that first-period interest amounts to $5,250 based on the original capital balance.

Capital Repayment Process

- The capital repayment is determined by subtracting interest from total payment:

- First-period capital repayment equals approximately $1,755.56.

- Remaining balance after this repayment is calculated as previous balance minus capital repaid; thus it becomes $223,244.44.

Summary Observations

Understanding Loan Amortization Methods

Overview of Loan Payment Structures

- As the loan progresses, interest payments decrease while capital repayments increase, maintaining a fixed monthly payment. The total repayment includes $225,000 in principal and an additional $196,333.58 in interest.

German Method of Amortization

- The German method features variable monthly payments with a fixed capital repayment amount. Borrowers know their monthly capital contribution upfront.

- Interest payments decline over time as the outstanding balance decreases, resulting in a constant capital repayment while interest fluctuates.

- To calculate the fixed capital payment, divide the total debt ($225,000) by the loan term (60 months), yielding a consistent monthly capital payment of $3,750.

- Interest is calculated on the remaining balance at an annual rate of 28%, divided by 12 for monthly calculations. This results in initial interest payments of $5,250.

- The first month's total payment combines both interest and capital contributions to equal $9,000; however, subsequent payments will vary due to decreasing interest costs.

American Method of Amortization

- The American method is less popular as it primarily involves paying only interest during most of the loan's life. Capital is repaid entirely in the final installment.

- Throughout most periods of this method, borrowers do not reduce their principal balance but pay only for borrowing costs until the last payment when they settle the entire principal amount.

- Monthly interest is calculated by multiplying the outstanding principal by the applicable interest rate divided by frequency (monthly).

- Fixed monthly interest amounts are established at $5,250 throughout most periods until reaching maturity when full principal repayment occurs.

Loan Amortization Systems: A Comparative Analysis

Overview of Loan Payment Structures

- The discussion begins with the identification that certain loan payment systems primarily involve interest payments, with no capital repayment. This raises questions about which system is most beneficial for borrowers seeking loans from banks or financial institutions.

Comparison of Amortization Methods

- A comparative analysis reveals that the American amortization system generates the highest interest payments, making it less desirable for borrowers. Consequently, this method is rarely sought after in practice.

- For borrowers, opting for a loan under the German amortization system is recommended as it incurs the least amount of interest compared to other methods.

Preferred Options Based on Perspective

- If one were to offer a loan instead of borrowing, choosing the American system would be advantageous due to its higher interest returns.

- The French amortization method serves as a middle ground between the German and American systems, balancing both lower and higher interest rates effectively.

Summary Insights