Decision Analysis in Venture Capital

Introduction

Clint Korver, a venture capitalist, discusses the decision analysis framework and the importance of telling the truth in venture capital. He also talks about his experience with pattern matching and uncertainty in the industry.

Decision Analysis Framework and Telling the Truth

- Clint learned fundamental frameworks from Ron that have been influential in how he practices venture capital.

- One of these frameworks is decision analysis, which will be discussed later.

- Another important framework for Clint is telling the whole truth, which has been influential in his work as a venture capitalist and in his personal life.

- This theme will be present throughout the talk.

Pattern Matching and Uncertainty

- When Clint first started in venture capital, he asked experienced VCs how to become a good VC. They told him it was all about looking at the entrepreneur and getting a feel for the market.

- However, Clint believed that there was more to it than just intuition and pattern matching.

- Venture capital is an extremely uncertain business with only 2% of VC dollars going to women-only teams last year.

- The top 100 investments out of 4000 deals account for all profits in the industry, making decision-making difficult.

Decision-Making Struggles in Venture

The speaker discusses the challenges of decision-making in venture capital, including uncertainty and ego, and how biases can be difficult to overcome.

Uncertainty

- Making investment decisions in venture capital involves a small number of data points and long time frames between making the decision and seeing the outcome.

- Decision analysis is used to confront ignorance with respect and dignity, allowing for a good risk-return view of the investment.

- Conversations with entrepreneurs are a mutual exploration of where the risk and value lie.

Ego

- Learning is key to confronting ego in venture capital. It involves having conversations with experts that allow for a good risk-return view of the investment.

- Diverse points of view are important to confront bias. Hulu Ventures brings together people with different backgrounds and perspectives.

Broken Social Feedback Loops

- Venture capital has broken social feedback loops on top of all its other challenges.

- Bringing in diverse points of view is the best way to confront bias.

Conclusion

The speaker concludes by saying that before discussing individual investment decisions, he wanted to give context about decision-making struggles in venture capital.

Venture Capital Investment Process

This section discusses the investment process of venture capital firms.

Steps in the Investment Process

- The first step is to figure out the firm's strategy, which involves deciding how to stand out among other venture capital firms.

- Once a strategy is established, the next step is to create a portfolio of investments that align with that strategy.

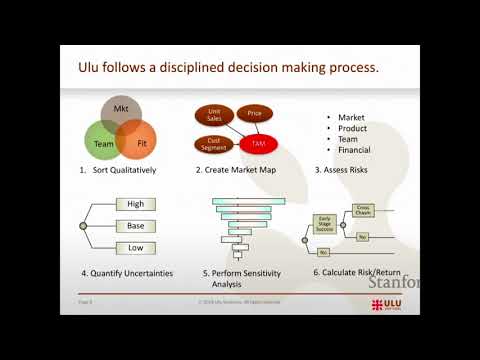

- To decide whether to invest in a startup company or not, Loulou Ventures uses a four-step process:

- Qualitative sorting: determining if the company fits their strategy and if they like the team

- Creating a market map: building a picture of the market opportunity

- Quantifying everything: bounding all assessments and doing sensitivity analysis

- Calculating an explicit risk return: pinpointing key issues and calculating risk-return ratio

Comparison with Other VC Processes

- Loulou Ventures' investment process is similar to most VC firms on step one. However, many VCs have less organized processes after that point.

Case Study: SoFi Social Finance

This section presents a case study of SoFi Social Finance, discussing how they identified an opportunity in student loans and created a successful business around it.

Background Information

- SoFi Social Finance was founded by Mike Cagney and his team from Stanford Business School in 2011.

- They identified an opportunity in student loans due to government regulation causing all banks to charge the same interest rates regardless of credit risk.

Business Model

- SoFi decided to cherry-pick customers with good credit scores from schools with low default rates and offer them lower interest rate loans.

- They focused on about 100 schools with a 1% or lower default rate.

- This business model allowed them to offer lower interest rates and still make a profit.

Success Factors

- SoFi's success was due to their ability to identify an opportunity in the market, create a unique business model, and execute it effectively.

- They were able to differentiate themselves from other lenders by offering lower interest rates to low-risk borrowers.

- Their focus on a specific niche market allowed them to build a strong brand and customer base.

Evaluating a Startup Investment Opportunity

In this section, the speaker discusses how they evaluated an investment opportunity in a startup called SoFi.

Criteria for Early Stage Success

- The team was great and hard to imagine a better team.

- They had already raised most of the two million dollars they were trying to put together further initial rounds.

- The product was interesting, but there was just missing a bit of execution on the product.

- Very high chance of early-stage success.

Crossing the Chasm

- Going from visionary customers to pragmatic customers is essential for crossing the chasm.

- There's probably a 70% chance that other schools would promote SoFi to their students.

- Various risks on the product and team could cause failure.

How to be a Mass-Market Player

In this section, the speaker discusses how to become a mass-market player and what it takes to succeed in a highly regulated environment.

Key Points

- The government may apply banking rules to non-bank companies that act like banks, which could kill their business model.

- There is a 60% chance of failure even if they get some top universities to adopt their program.

- A 40% chance of success has to be attractive enough to make up for the 60% chance of failure.

Calculating the Value of Success

In this section, the speaker talks about how they calculate the value of success and assess dilution.

Key Points

- Ownership depends not only on the valuation but also on future dilution that might happen.

- Entrepreneurs are not very good at assessing dilution, so they rely heavily on benchmark data.

- Mass market share is a key driver of risk and value. A three percent market share would result in less than 10x probability-weighted multiple on invested capital, while a 30 percent market share would result in around 50x probability-weighted multiple on invested capital.

Bottom Line Chart

In this section, the speaker brings everything together and presents the bottom line chart.

Key Points

- If you're a market leader with a two percent shot at success, you could generate about $1.6 billion in revenue with an enterprise exit value of $9 billion.

Investment Criteria

This section discusses the criteria for investment and how to determine if a company is investable.

Determining Investability

- The bottom line number is 10x or better to be considered investable.

- The goal of this exercise is not to come up with the right answer, but clarity of action.

- At 20x, there can be some room for error, but at 9.8x, everything needs to be believed.

- It's harder to invest at 9.8x because even a small deviation in the high or low range could change the outcome significantly.

Market Opportunity

This section discusses market opportunity and how it affects investment decisions.

Filtering Companies

- One thing they look for when doing due diligence on a company is whether they are playing in a big enough market opportunity.

- They don't look at timing when determining early stage success because it's hard to predict innovation waves.

- If a company never gets out of the gate and has no customers, it's easy to see that something was missed.

Learning System

This section discusses their learning system and how they use it to improve their investment decisions.

Improving Investment Decisions

- They have built a learning system so they can compare what actually happened versus what they expected would happen.

- If something goes wrong with an investment, they use their learning system to figure out what went wrong and how to improve their investment decisions in the future.

Funding Arrangements

In this section, the speaker discusses funding arrangements and probability distributions.

Trade-offs in Probability Distributions

- The speaker's team explores funding arrangements that change the probability bands around what they might get.

- This gives them a trade-off because they have a number at the end which they know without a probability distribution.

Outlier Driven Investments

- The speaker's fund is outlier driven, meaning that somebody being in a certain category makes their entire fund.

- They are reluctant to do anything that reduces the topside possibilities even if it can shore up the bottom.

Portfolio Construction

In this section, the speaker talks about portfolio construction and how they decide on ownership percentage or stake.

Ownership Percentage vs. Probability Weighted Multiple

- The speaker's team is different from typical VCs who build their whole story for investors around ownership percentage.

- For them, 1% of Google works just fine as long as they're getting a good multiple.

- Follow-on investments to maintain ownership percentage is not important for them.

Learning Process

- Early on, experts in the industry said that doing reference checking and looking at customers' feedback was a waste of time.

- However, the speaker's team did it anyway based on their gut feeling.

- They learned from their 60 company portfolio but still believe in doing reference checking.

The Importance of a Systematic Process

In this section, the speaker discusses the importance of having a systematic process when evaluating companies for investment.

Benefits of a Systematic Process

- A systematic process helps to identify all risk factors and prevents investors from falling in love with companies.

- Confirmation bias can be avoided by using a systematic process.

- Initial data suggests that using a systematic process leads to better decision-making.

- Companies invested in using the process have a much lower failure rate compared to those not using it.

Market Conditions and Portfolio Performance

In this section, the speaker talks about market conditions and how they affect portfolio performance.

Market Conditions

- The venture business has been great since 2008 due to an influx of money into the industry.

- SoftBank Fund has $91 billion to invest in late-stage companies.

- Many companies in their portfolio are propped up by money and will eventually fail.

- SoFi is doing well despite underestimating dilution.

Portfolio Performance

- SoFi did $500 million in revenue last year and is hugely profitable.

- Dilution can be beneficial as it provides more opportunities for success.

- Mike was successful because he was not stingy with equity when pulling in capital.

- Portfolio construction is important but often poorly done in venture.

Portfolio Construction

In this section, the speaker discusses portfolio construction and its importance in venture.

Portfolio Construction

- Portfolio construction refers to the number of investments in a portfolio and how much is held for follow-on investments.

- Industry averages suggest that for every $1 invested, $0.50 is held for follow-on investments.

Investing in Startups: Picking Winners

This section discusses the idea of picking winners in the startup industry and why it is a fool's errand.

No One Picks Winners

- John Doerr, Mike Moore, and Doug Leone are famous names who have had successes but also many failures.

- Even with successful investors like John Doerr, there are still more failures than successes.

- The probability distribution over returns for early-stage venture is described as a power law with a few huge returns pulling up the mean even though the median looks pretty normal.

- Late stage VC has less of this dynamic but still only looks about half the returns on the mean side.

Large Portfolio and Early Stage Investment

- To get outlier success, you need to put your money upfront when you can buy a lot of ownership.

- A large portfolio is necessary to account for uncertainty and increase chances of success.

- Early-stage venture has a higher mean return compared to late-stage venture.

- Investing in every single venture investment done would give you the mean by definition.

Portfolio Size and Outliers

In this section, the speaker discusses how big a portfolio needs to be to feel confident about giving investors high-quality returns.

Chance of an Outlier

- The speaker explains that they have good sourcing and a process that gives them an average 4.5% chance of an outlier every time they write a check.

- They compare their chances with those of top-tier VCs and show a graph with the blue line representing top-tier VCs and the red line representing average VCs.

- At 50 investments, they have roughly a 90% chance of an outlier, but there is still a 10% chance of mediocre results due to bad luck.

- The goal is to get as close to 100% as possible.

Concentrated Portfolio vs Large Portfolio

- The typical VC story is that they can pick winners, so they have a concentrated portfolio with around ten investments.

- However, this strategy only has a 20% shot at having an outlier in their portfolio.

- The speaker emphasizes that it's not just about one fund with great returns but rather a series of funds with great returns.

- With fifty investments, there is a 73% chance of three funds in a row with outliers.

Qualitative Factors

- There are some qualitative factors to consider when constructing portfolios such as sourcing and selection processes.

- Their selection process takes two days but can only be done for limited amounts.

- They aim to support their investments from seed to series A and roll off the board when Sequoia comes in and leads the series A.

Doubling Down on Winners

In this section, the speaker talks about doubling down on winners in venture capital.

Followings

- Almost everybody in the industry believes that doubling down on winners is the key to success.

- However, only 2% of VCs believe in their story of large portfolios and doubling down on all investments.

- The speaker mentions a fund-to-fund that came to them and said they don't understand portfolio construction.

Investing Capital Upfront

In this section, the speaker discusses investing capital upfront and how it can lead to better returns.

Investing Capital Upfront

- The speaker suggests putting all the money into the seed round across winners and losers.

- This leads to buying 12.5% of each company in the seed round as opposed to 3.3%.

- The fund of funds argues that not following on in series A, B, and C will lead to dilution.

- However, investing all the money upfront leads to twice the ownership in best companies that have survived.

Opportunity Cost

In this section, the speaker talks about opportunity cost and how every dollar invested has to compete with every other place where investment could be made.

Opportunity Cost

- Every dollar invested has to compete with every other place where investment could be made.

- If a Series A investment is better than 10x, then they invest; otherwise, they think about it.

- About a third of their companies get to follow-on Series A in that 10x or better category.

Portfolio Management

In this section, the speaker discusses portfolio management and how many investments they make at different stages.

Portfolio Management

- They have made 27 investments in Fund II (64), Fund I (27), and Fund III (not mentioned).

- They are on three boards each so eight boards out of thirty call it.

- They rely on other people to be essentially the governance and watch out for their interest.

- Seed stage is nicely constructed for that in the sense that most of these seed rounds are like a million to two million dollars, and there's probably two or three or sometimes even four venture firms like them that are writing five hundred thousand dollar checks in that.

Investment Expenses and Follow-Ons

In this section, the speaker discusses the expenses associated with investments and the work involved in follow-ons. They also talk about the balance between risk-return and volume.

Investment Expenses

- Each investment has expenses associated with it, mostly on the time side.

- Building relationships with investors can be time-consuming.

- Doing follow-ons is a lot of work but less than initial investments since there is already a framework in place.

Risk-Return Balance

- Lowering standards to invest in more companies would require a much bigger portfolio.

- Investing $100 in every early-stage company would be a smart strategy if access was available to all reputable venture firms.

- Access to the best deals is competitive, so entrepreneurs need to understand why having Alou as an investor is valuable.

Future Plans for Alou Ventures

In this section, the speaker talks about future plans for Alou Ventures, including automating some processes and creating self-service venture capital. They also discuss their meaningful purpose initiative.

Automation and Self-Service Venture Capital

- The goal is to automate some processes currently done through performance art (whiteboard presentations).

- Self-service venture capital could allow for more efficient evaluation of potential opportunities.

Meaningful Purpose Initiative

- Entrepreneurs come with a huge amount of purpose, which aligns with Alou's values map.

Signature Events in Life and Venture Capital

In this section, the speaker talks about signature events in his life and what gives him energy. He also discusses how he spent 15 years before realizing that he was bad at repeatable entrepreneurship.

What Gives Energy

- The speaker gets a lot of energy from looking at the next possibility, which is why venture capital is a spectacular business for him.

- The conceptualization of what's the problem that customers have and are they willing to pay for it, how to get product market fit, and convince those first couple of customers to buy my product gives him unstoppable energy.

Repeatable Entrepreneurship

- The speaker got four companies up to a million or a few million dollars in revenue but nothing happened after that because he was bad at repeatable entrepreneurship.

- From an intellectual point of view, decision analysis and venture drives the speaker right now. He has had enough success in this area to feel like he has a platform for doing more.

Data in Venture Capital

- A group of folks are forming around data in venture capital, including GV (Google Ventures), correlation ventures, and others.

- The speaker believes that data and models are such a better way to do things than relying on smart guys making decisions. He thinks venture capital could follow the same route as public equities where data dominates the field.

Company Outcomes Software Failure

In this section, the speaker talks about one category of failures - company outcomes software failure - using his own experience with Outcome Software as an example.

Outcome Software

- Outcome Software was going after risky recurrent decisions in big enterprise, such as which products to launch in which countries.

- The company had the very first internet-based system that pulled data out of ASAP system on my cost data and then used it to help customers make better decisions.

Enterprise IT Category

In this section, the speaker talks about their experience in enterprise software and how they chose to focus on this category for their venture capital firm. They also discuss the limitations of consumer markets.

Choosing Enterprise IT Category

- The speaker's expertise is in enterprise software, so it was easy to gravitate towards that when they started doing venture capital nine years ago.

- Consumer markets are hard to model given the level of expertise required to identify what is "cool" and will have monstrous adoption.

- The speaker believes that they have a fighting chance at figuring out whether an enterprise product is representative of industry needs and can sell through distribution channels.

Limitations of Consumer Markets

- The speaker's 18-year-old daughter can spot "cool" from a mile away, but the speaker had a hard time picking out cool before it actually popped.

- As soon as something explodes in consumer markets, it's easy for everybody to see that they want to be an investor.

Fundamental Flaw in Selling into Enterprises

In this section, the speaker discusses a fundamental flaw in selling into enterprises and how it affected one of their most successful companies.

Two Yeses Inside Each Enterprise

- To launch a product within an enterprise, both finance and business unit managers would need to say yes.

- Getting two yeses from two different silos within an enterprise is difficult and often leads to nightmares.

Decision Quality International

- Decision Quality International was the speaker's most successful company with promise.

- The company sold training materials to big enterprises on how to make high-quality decisions.

- Training is a fabulous business model, especially when an organization wants to train thousands of people.

Strategic Mistake

In this section, the speaker talks about a strategic mistake they made in one of their ventures.

Strategic Mistake

- The speaker's venture had to get two yeses from two different silos within an enterprise.

- Selling into multiple silos within an enterprise was a nightmare and a strategic mistake.

- The speaker believes that they have a fighting chance at figuring out whether an enterprise product is representative of industry needs and can sell through distribution channels.

Consumer Engagement as a Candidate

In this section, the speaker discusses how consumer engagement is a great candidate for investment but requires some investments in figuring out the right distinctions.

Consumer Engagement

- Consumer engagement is a great candidate for investment.

- The distinction between users who use an app for an hour a day versus those who use it for only a couple of minutes per month is important to consider.

- It doesn't work well when nobody has any expertise.

Decision Analysis in Pharmaceutical R&D and Oil and Gas

In this section, the speaker talks about decision analysis being best practice in pharmaceutical R&D and oil and gas industries.

Decision Analysis

- Decision analysis is best practice in pharmaceutical R&D and oil and gas industries.

- Decision analysis shows up as being very important when there's lots of uncertainty.

- The model is designed to handle critical mass on both sides of the marketplace.

Critical Mass in Marketplaces

In this section, the speaker discusses critical mass in marketplaces.

Critical Mass

- Crossing the chasm of the marketplace is what critical mass means.

- Diversity is one of their investment thesis.

- Systemic bias creates opportunity for them to systematically look at diverse groups.

- About 30% of their CEOs are women compared to 5%-8% women CEOs in other companies.

- Two of their best outcomes are from Latino entrepreneurs.

Diversity and Investment Strategy

In this section, the speakers discuss their investment strategy and how it relates to diversity.

Raising the Floor vs. Raising the Ceiling

- Miriam is focused on diversity and wants to raise the ceiling for diverse entrepreneurs.

- Other investors, such as Courtney at Cal Kapur Capital, are focused on raising the floor.

- The debate centers around whether it's more important to invest in raising the floor or raising the ceiling.

Follow-On Investment Strategy

- The volume of investments drives success in finding an outlier.

- Once an outlier is found, follow-on investments maximize returns.

- There isn't a specific number of investments needed for success; it's more about the relationship between investments.

When to Use Follow-On Investing

- Follow-on investing can be a smart strategy if you're terrible at selecting successful investments or negotiating terms.

- If you're not good at seed stage investing, don't do it.

Conclusion

The speakers thank each other for coming and offer to share slides from their presentation.