Session 3A: The Balance Sheet (Examples)

Understanding Balance Sheets Across the Corporate Life Cycle

The Young Company Stage

- A young company's balance sheet typically shows minimal debt, reflecting its limited history and asset base.

- Shareholders' equity can be negative due to ongoing losses; this is common for young growth companies.

- As a company grows, it may receive equity infusions from venture capitalists or public offerings, potentially turning equity positive despite not yet being profitable.

Transitioning to High Growth

- In the high growth phase, the asset base expands significantly while maintaining low debt levels.

- Mature growth companies see stabilization in their asset base and an increase in debt as they begin generating profits.

Mature Stable Companies

- Mature stable companies often have large and growing debts; shareholders' equity may decline if substantial cash returns are made through dividends or stock buybacks.

Case Study: Peloton's Early Life Cycle

- Peloton's balance sheet reflects its youth with a small but rapidly growing asset base of $271 million to $865 million.

- Negative shareholders' equity indicates ongoing losses; cash and marketable securities represent its largest assets, though future growth potential isn't captured on the balance sheet.

Case Study: Netflix's Growth Phase

- Netflix’s biggest asset is non-current content costs, highlighting the importance of intangible assets in its valuation.

- Deferred revenue appears as a current liability since Netflix collects subscription fees upfront but must provide services over time.

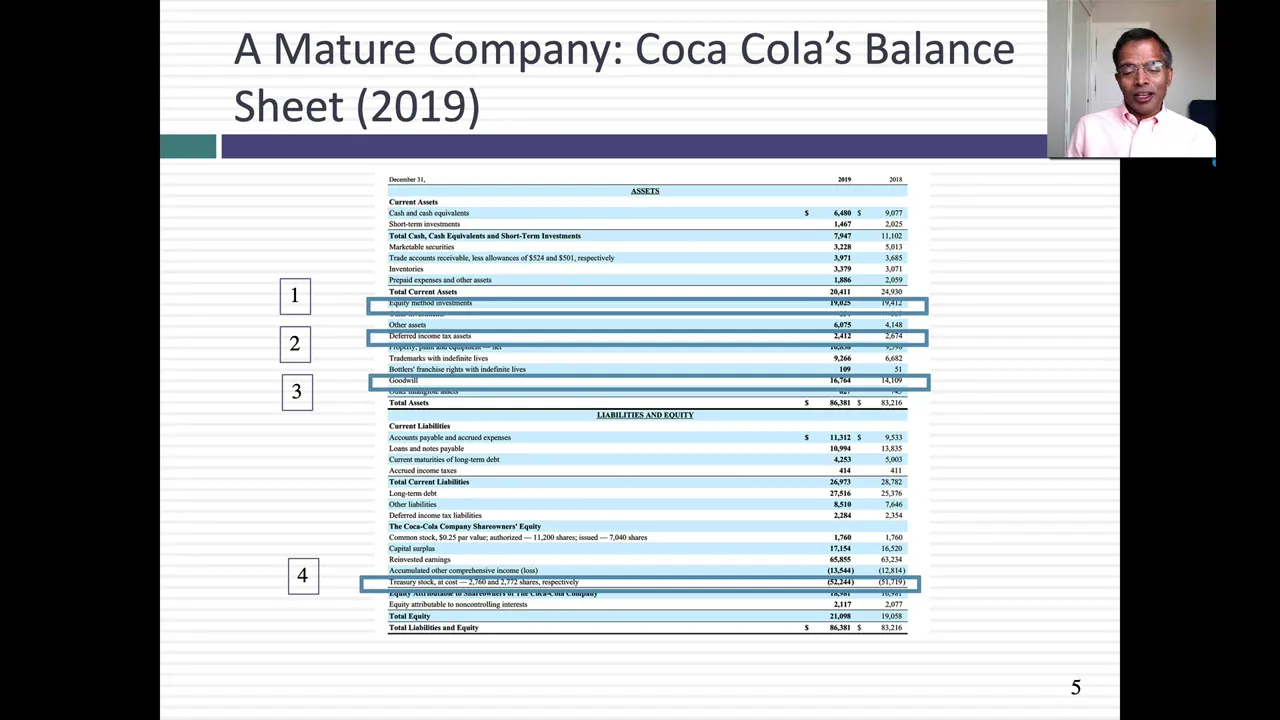

Case Study: Coca-Cola's Maturity

- Coca-Cola’s balance sheet shows a significant asset base that isn’t growing quickly, indicative of maturity.

Understanding Coca-Cola's Financial Statements

Tax Assets and Future Implications

- Coca-Cola's tax assets indicate overpayment in previous years, leading to reduced future tax liabilities. This does not imply immediate cash availability from liquidating the company.

Goodwill and Its Significance

- Goodwill on Coca-Cola's balance sheet reflects past acquisitions at high prices but provides little meaningful insight into the company's current value.

Treasury Stock and Share Buybacks

- When Coca-Cola repurchases shares, it can either hold them as treasury stock or cancel them. Holding shares allows for future issuance, while cancellation reduces outstanding shares.

- Currently, Coca-Cola is holding its repurchased shares as treasury stock, which impacts book equity by depressing shareholders' equity due to buybacks.

Debt Breakdown and Forecasting Cash Flows

- The footnotes of Coca-Cola’s financial statements provide a breakdown of debt by currency, maturity, and coupon rates—essential for forecasting cash flows.

- The book interest rate listed is not the cost of debt; it represents the promised rate at borrowing time.

Intangible Assets: A Closer Look

- Despite being a major brand, Coca-Cola’s balance sheet lacks significant intangible asset representation like brand name; goodwill dominates their intangible assets.

- Other intangibles such as customer relationships are minor compared to the company's overall valuation (around $200 billion), indicating a disconnect between accounting practices and actual brand value.

Analyzing Toyota's Financial Statements

Characteristics of a Mature Company

- Toyota’s balance sheet indicates maturity with stable total assets and revenues.

Finance Receivables as an Asset

- Toyota includes finance receivables from its captive bank that loans money for car purchases within current liabilities.

Investments in Affiliated Companies

- Similar to Coca-Cola’s investments, Toyota lists affiliated companies as assets reflecting investments made without trading intentions.

Pension Liabilities Across Countries

- Accrued pension costs may vary by country; underfunded plans must be shown as debt in some regions but not others (e.g., Germany vs. U.S.).

Deferred Income Taxes: An Indicator of Past Payments

Understanding Sector-Specific Financial Statements

Overview of Sector Differences in Financial Reporting

- The discussion begins with an examination of sector-specific line items in financial statements, focusing on three sectors: commodities, financial services, and pharmaceuticals.

- In the commodity sector, particularly oil companies, inventory is highlighted as a significant item that can fluctuate dramatically in value based on market prices.

- An example illustrates how oil extracted at $60 per barrel may lose nearly half its value if the market price drops to $35 by mid-year.

- Unlike manufacturing companies where inventory typically retains its value, commodity inventories are subject to rapid depreciation due to market volatility.

Currency Translation Adjustments and Liabilities

- The concept of currency translation adjustments is introduced; these reflect foreign exchange gains or losses that can appear either on the income statement or directly on the balance sheet as part of shareholders' equity.

- Employee benefits are discussed as liabilities on balance sheets, emphasizing their importance for companies like Toyota.

Insights from Banking Sector Balance Sheets

- HSBC's balance sheet reveals a predominance of financial assets, which are easier to assess for market value compared to physical assets.

- The practice of mark-to-market accounting is noted as a long-standing trend in banking due to the nature of its assets.

- Non-controlling interests are explained as accounting estimates reflecting ownership stakes not fully owned by the reporting entity.

Pharmaceutical Companies and Intangible Assets

- Dr. Reddy's Labs serves as an example where valuable patents developed through R&D do not appear prominently on the balance sheet despite being critical assets.

- Goodwill and other intangible assets often overshadow more significant intellectual property like brand names and research developments.

Evolution and Challenges in Balance Sheet Accounting

- A key takeaway is that balance sheets represent a company's historical financial position but face challenges due to differing accounting practices across sectors.

- There’s ongoing debate among accountants regarding whether balance sheets should reflect actual investments or fair values of assets today.

- Current practices result in confusion within balance sheets—neither purely reflecting capital invested nor fair values effectively.