8. ¿Dónde están los beneficios que no los vemos?

Recordad: la cuenta de resultados y la tesorería

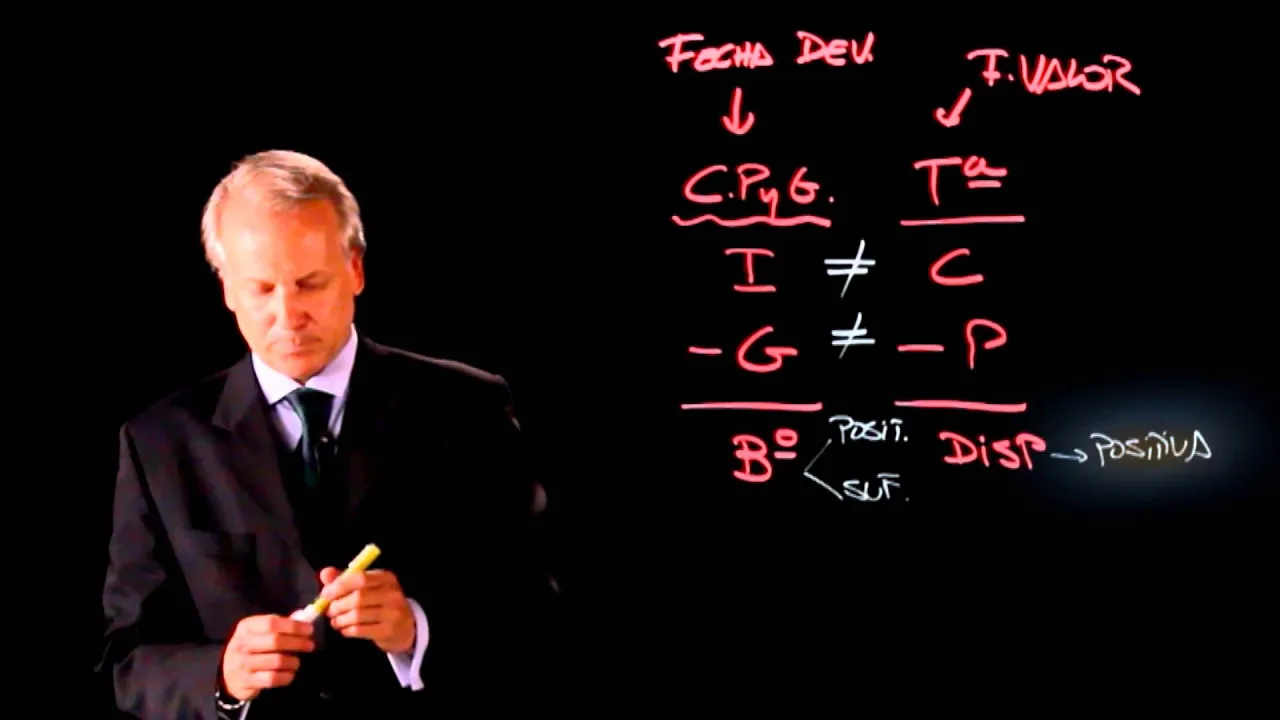

In this section, the speaker emphasizes the distinction between the income statement and cash flow statement, highlighting that revenues and expenses are not equivalent to receipts and payments.

Understanding Revenues and Expenses

- Revenues minus expenses form the basis of the income statement.

- Income is not synonymous with receipts, and expenses do not equate to payments.

Misconceptions on Weekend Expenditure

- Purchasing a season ski pass for 400€ raises questions about categorizing weekend expenditures.

- Distinguishing between weekend expenses like milk purchases and seasonal ski pass payments is crucial for accurate financial analysis.

Importance of Proper Expense Allocation

- Allocating each expense to its respective consumption period ensures accurate financial analysis.

- While cash flow analysis is vital, it should be kept separate from income statement analysis for clarity in financial management.

Key Elements in Business Viability

This segment delves into essential factors determining a company's viability, focusing on profitability and positive cash flow as fundamental requirements.

Profitability and Cash Flow

- Two critical variables for business viability are positive and sufficient profits along with positive cash flow.

- Profitability alone does not guarantee viability; positive cash flow is equally crucial to ensure operational sustainability.

Significance of Cash Flow Management

- A profitable company may face liquidity issues if cash inflows are delayed or customers default on payments, underscoring the importance of maintaining positive cash reserves.